India Budget Report (AKM Global Corporate Advisors)

Business Opportunities

September 17, 2024 - AKM GlobalThe Indian Union Budget 2024, introduced key tax proposals, including several that impact foreign companies operating in or with India. Member firm AKM Global has summarized the major changes in the following thought leadership article.

Access our Business Opportunities Insights hub to access similar articles about international business and global opportunities.

The Indian Union Budget for 2024 had several important tax proposals. This was supposed to be a pathbreaking budget exercise considering that this was the first budget after the current dispensation managed to form the government with a relatively less favorable mandate than last time.

Among these, there are several amendments which are relevant for foreign companies doing business with or in India.

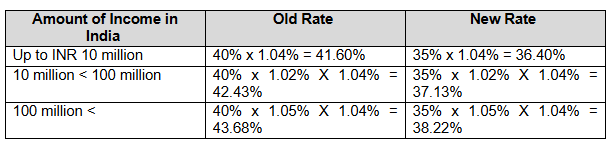

Reduction in Tax Rate for Foreign Companies

The foreign companies operating in India are subject to tax rate of 40%. This tax rate has been reduced to 35%. Hence, the incomes are not otherwise subject to a special rate (like capital gains) are subject to a tax rate of 35%. Apart from these, the incomes are subject to a surcharge (depending upon the level of income) and mandatory cess @ 4%. Hence, the final tax rate depending upon the level of income are tabulated below.

Withdrawal of Equalisation Levy

Pending finalisation of Pillar 1 and Pillar 2 solutions and pursuant to the interim measures suggested in BEPS Action Plan 1 for Tax on Digital Services, India introduced Equalisation levy @ 6% in 2016 when it was first introduced on foreign MNEs providing online advertising services to the Indian businesses. The Indian companies paying these fees were supposed to remit the fee after deducting 6%. Further, the levy was introduced under a different statute and not as part of the principal statute dealing with taxation on income, hence it was not subject to tax credit under Double Taxation Avoidance Agreements (‘DTAA’ or ‘tax treaty’) or in some cases even unilaterally, the home jurisdiction of these MNEs.

In 2020, the scope of this levy was widened significantly wherein a levy of 2% was made payable by foreign MNEs on providing services in the nature of e-commerce. The word ‘e-commerce’ was defined very widely wherein it covered all services (or even a part of services) provided through digital modes to be covered under the levy. However, those services would still be out of ambit if the services are subject to withholding in India due to classification of those services as a Fee for Technical Services (FTS or Royalty or if the foreign enterprise has a Permanent Establishment (PE) in India and the income is attributed to that PE.

As a major relief this 2% levy has been withdrawn from 1st August, 2024 and hence the foreign MNEs providing such services would not be required to pay this levy.

Change in Tax Treatment of Buyback

Many Indian companies used the route of buyback to distribute the profits/capital to investors by taking a tax arbitrage as buyback attracts a tax rate of 20%. Now the companies are relieved from this payment of tax. Previously, the tax liability was @20% of the buyback amount which means the consideration paid by the company less the amount received by the company for issue of such shares. Now the amount received from the company towards buy-back of shares would obtain the character of dividend, the gross amount would be taxable as dividend under the head "other sources". It means now the shareholders are exposed to dividend Income and the cost of acquisition would partake the character of capital loss. The said amount may be a long-term or a short-term capital loss based on the period of holding of the shares. This has been amended to the effect that it shall be treated as dividends henceforth and hence shall be subject to treaty relief and tax credit in home jurisdiction.

Further the companies undertaking buy back will be able to take a deduction related to inter-corporate dividends under section 80M of the act.

Overhaul of Capital Gains

Changes has been proposed in the capital gains tax regime as tabulated below.

Further the concept of indexation has completely proposed to be removed which means that foreign investors will no longer be able to adjust their cost of acquisition for inflation when calculating long-term capital gains. This could result in a higher taxable gain and, consequently, a higher tax liability, particularly for assets held over long periods. This change might affect the attractiveness of long-term investments and alter the investment decisions of foreign investors.

Also, there is enhancement in the exemption limit of long-term capital gains from Listed equity shares, Units of equity oriented mutual fund and units of business trusts from INR 1,00,000 to INR 1,25,000. While this provides some relief and may slightly reduce the tax burden for gains up to this threshold, it might not significantly offset the impact of increased tax rates and the removal of indexation.

This will impact the foreign investors having strategic or portfolio investments in India.

Withdrawal of Angel Tax

Angel tax is applicable on unlisted companies on the capital raised through the issue of shares Introduced in 2012 as anti-abuse measures to deter the generation and utilization of unaccounted money. The angel tax was attracted to privately held companies raising capital at a value above fair market value (DMV). Consequently, the amount by which issue price exceeds the FMV, is considered as the income of such privately held companies. The provision used to apply to the capital raised from Indian resident investors or promoters (barring certain VCs), however, its ambit was extended the capital raised from overseas investors as well in the year 2023.

Since its inception, the provision attracted several litigations wherein the valuations were often challenged by the tax department particularly in case of start-ups. Much of the energy and resources used to get spent in responding and fighting those litigations. The Central Board of Direct Taxes (CBDT i.e. the board which looks after the administration of Corporate tax in India) and the government issued several relaxations and clarifications to accentuate those but these didn’t prove very effective in bringing down the volume of litigations.

As a welcome move, this provision has altogether been done away with and hence the amount raised at a valuation above the FMV will no longer be considered as income for the privately held companies. This is sure to bring relief and bring down the controversies and litigations, but it remains to be seen whether the tax department may try to tax these under any other existing provisions.

Other measures for Litigation Management

Expanding the Scope of Safe Harbour Rules: The Safe Harbour rules under transfer pricing provisions in India are set to be expanded to make them more attractive for multinational corporations (MNCs) operating in the country. These rules determine the circumstances under which income tax authorities will accept the transfer pricing declared by taxpayers. Originally introduced to ease compliance for smaller taxpayers and low-value transactions, reduce transfer pricing litigation, and clarify arm's length pricing, the rules have not seen significant adoption due to their restrictive nature and high mark-ups prescribed. The Union Budget 2024 addresses these concerns by announcing plans to enhance and broaden the Safe Harbour rules, with specific details yet to be provided. Additionally, a new Safe Harbour rate will be introduced for foreign mining companies selling raw diamonds in India to support the diamond cutting and polishing industry.

This initiative is a commendable step towards simplifying transfer pricing provisions and reducing litigation in India. It is expected to be well-received by multinational corporations seeking relief from the numerous transfer pricing challenges they frequently face. This move is likely to booster investor’s confidence and encourage exploration of further opportunities in the expanding Indian market.

Reforming Tax Dispute Resolution (VsV): To expedite the resolution of appeals and settle disputes with reduced interest and penalties, Union Budget 2024 has proposed the Vivad Se Vishwas (VsV) Scheme, 2024. Originally launched in 2020, the scheme received a positive response from taxpayers and significantly contributed to government revenue. Building on the success of the 2020 scheme, the 2024 version is designed to address tax disputes and reduce litigation while boosting revenues. The 2024 scheme also extends to appeals pending before the Dispute Resolution Panel (DRP), which includes transfer pricing cases and appeals involving foreign companies.

To further mitigate tax-uncertainty and disputes, the Union Budget 2024 proposes a thorough simplification of reassessment, including a reduction in reassessment time limits. As a result, an assessment hereinafter can be reopened beyond three years from the end of the assessment year only if the escaped income is Rs 50 lakh or more, up to a maximum period of five years from the end of the assessment year. This reduction brings increased certainty to taxpayers by limiting the duration during which past assessments can be reviewed, thereby enhancing overall taxpayer confidence.

These measures aim to make the tax litigation process more efficient and less burdensome for both taxpayers and the tax administration system.

Increase in Monetary Threshold for Appeals to Curb Unnecessary Tax Litigation: To address the backlog of unnecessary appeals pending at various forums, the Union Budget 2024 proposes raising the monetary limits for filing appeals with higher tax authorities if the tax effect in the case does not exceed the specified threshold.

It has been proposed to increase monetary limits for filing appeals related to direct taxes, excise and service tax in the Tax Tribunals, High Courts and appeals/SLPs before Supreme Court to Rs 60 lakh, Rs 2 crore and Rs 5 crore, respectively. The earlier mone

ary limit for moving to Appellate tribunal, High courts and Supreme court was Rs 50 lakh, 1 crore and Rs 2 crore, respectively.

This aims to ensure that only cases with significant tax implications are escalated further by tax authorities thereby preventing filing of unnecessary appeals by tax authorities.

Duty Measures

Reduction of duty to 15% on mobile phones, mobile PCBAs, and chargers: The Indian government’s recent budget announcement to reduce duties on mobile phones, mobile Printed Circuit Board Assemblies (PCBAs), and chargers to 15% marks a significant step towards fostering a more conducive business environment for foreign entities. With reduced import duties, foreign entities can provide more competitive pricing, giving them a significant edge in the Indian market. This increased competitiveness allows for greater market penetration and the potential to capture a larger share of one of the world’s fastest-growing mobile phone markets. Lower import costs mean that foreign entities can offer more competitively priced products in the Indian market, which is vital in a price-sensitive and rapidly growing market. Foreign entities are now in a better position to explore strategic partnerships with local firms. Collaborations with Indian companies can provide valuable insights into the domestic market, help navigate regulatory requirements, and leverage established distribution networks.

Reduction of duties on gold and silver: The recent reduction in custom duties on gold and silver by the Indian government presents a transformative opportunity for foreign investors. This significant reduction lowers the cost of importing these precious metals, making India an increasingly attractive market for international entities involved in mining, refining, and trading. Foreign entities stand to benefit greatly from the reduced operational costs, which directly translate to higher profit margins. With the lower import duties, these entities can offer more competitive prices within the Indian market. This enhanced competitiveness not only helps in increasing market share but also in establishing a stronger presence in one of the world's largest markets for gold and silver. Moreover, the reduction in duties creates a favourable environment for new investments, encouraging foreign players to explore strategic partnerships with local firms. These collaborations are invaluable, providing deep insights into local market dynamics and aiding in navigating the complex regulatory landscape.

Full exemption from customs duties on 25 critical minerals, including lithium, copper, cobalt, and rare earth elements: The Indian government’s recent budget announcement to grant full customs duty exemption on 25 critical minerals, including lithium, copper, cobalt, and rare earth elements, marks a significant strategic shift in its economic policy. This exemption dramatically reduces the cost of importing these essential resources, directly lowering operational costs for foreign entities involved in high-tech production and manufacturing. With minimized import expenses, companies can achieve higher profit margins, making their operations in India more financially attractive. This policy change is expected to stimulate substantial foreign investment in India's high-tech manufacturing sectors. The availability of critical minerals at lower costs encourages companies to establish manufacturing units in India, aligning with the government's vision of making India a global manufacturing hub. Increased investment will spur market growth, create jobs, and drive technological advancements. Access to affordable raw materials like lithium, copper, cobalt, and rare earth elements is vital for the development of cutting-edge technologies in sectors such as electronics, renewable energy, and electric vehicles. The duty exemption supports innovation and technological advancement, reflecting a stable and supportive policy environment for high-tech industries in India. Foreign entities can undertake long-term strategic planning with greater confidence, knowing that the government is committed to fostering growth and innovation in these sectors.

GST Litigation Rationalisation

Waiver from interest and penalty for FY 2017-18 to FY 2019-20 in bonafide cases: The Indian government’s recent budget announcement to waive interest and penalties for the fiscal years 2017-18 to 2019-20 in bonafide cases marks a significant and strategic move aimed at fostering a more favourable business environment. Foreign entities often struggle with the GST implications of cross-border transactions, including import and export of services. Misinterpretations of tax liabilities can result in unexpected dues. The waiver allows entities to address these issues comprehensively, ensuring compliance and correcting past errors. The constant evolution of GST compliance requirements, such as e-invoicing and new return filing systems, can lead to inadvertent lapses in compliance. The waiver provides a relief window for entities to update their systems and processes to align with current requirements.

The above tax proposals are expected to rationalize the overall tax regime in India and as is visible, the focus seems to be on the reduction of tax controversies and litigations and make the tax regime simpler. In another major announcement, it has also been proposed that the income tax law in India shall be considered for an overhaul with the aim of making it simpler and reducing the litigations. The government aims to complete the exercise within next 6 months which reflects the aforesaid intent.

Content by:

AKM Global

Headquartered in Delhi NCR, India, AKM Global is a full-service firm providing tax and consulting services to clients ranging from Fortune 500 corporations to startups and high-net-worth individuals. With a team of over 900 professionals operating out of 7 locations, the firm combines deep technical expertise with extensive experience in international tax, regulatory, financial, and economic matters to deliver practical, business-focused solutions. AKM Global's industry experience spans over 45 years, and they provide a wide spectrum of cross-border transactions, which include but are not limited to international tax planning, transfer pricing, double taxation relief, expatriate tax services, or cross-border M&A tax assistance, due diligence, foreign exchange controls, audit support, corporate law, litigation, outsourcing, and EOR services etc. By bringing tax-efficient and pragmatic solutions that maximize global opportunities while minimizing risks, AKM Global is fueling the growth of its clients. With an exceptional global network and working relationships with reputed accounting and law firms across the world, AKM Global can address cross-border tax complexities across diverse jurisdictions. While the current practice is expanding, the relatively new business verticals such as White-collar crime defence practice has received exceptional feedback from the clients. Under this area of practice, AKM Global is handling cases involving clients facing actions from different law enforcement agencies such as the Enforcement Directorate, CBI, Income Tax (under the Income-tax Act, Black Money Act, Benami Law), Customs and GST, Serious Fraud Investigation Office, etc which can be attributable to inter-agency intelligence sharing and coordination. From 2017 through to 2026, AKM Global has been consistently ranked as a leading Tax and Transfer Pricing Firm in the World Tax Guide and the World Transfer Pricing Guide by International Tax Review. Additionally, the company has been nominated in various tax award categories, including “India Transfer Pricing Firm of the Year”, “Global Executive Mobility Tax Firm of the Year”, “India Transfer Pricing Firm of the Year and “Tax Compliance and Reporting Firm of the Year”, since 2016 under the prestigious Asia Tax Awards organized by ITR. The firm's partners are regularly featured as subject matter experts on International Tax, Transfer Pricing, and Exchange Control Regulations across leading television channels and prominent domestic and international publications. Their insights and expert commentary have appeared in renowned media outlets, including The Economic Times, Business Standard, Financial Express, The Indian Express, Reuters, Financial Times (UK), Tax Analysts (US), CNBC, ET NOW, and others.

Learn more