Real Estate Tax Reform - Implementing Housing Justice in Taiwan (Chungsun Prime CPA LLP)

Business Opportunities

November 29, 2022This is a thought leadership article by Chungsun Prime CPA LLP, examining the steps taken by the Taiwan Ministry of Finance (MoF) to clamp down on property tax evasion and excessive speculation in the real estate market.

If you would like to submit an article that highlights insightful thought leadership content from your firm, and you are industry experts in your field, you can do so here.

The Taiwan Ministry of Finance (MoF) has taken steps to clamp down on property tax evasion and excessive speculation in the real estate market. The headline changes are longer holding periods, but details like changes to deductions and an expanded scope could have a large impact on property transactions.

Overview

Capital gains tax revisions came into force on 1 July 2021, with the changes applying to property transactions from 1 January 2016. The revisions increase the progressive tax rate, extends the scope of the tax, and reduces deductions when calculating capital gains.

The MoF issued this change to prevent excessive speculation in the property market, following a period of low interest rates fueling easy access to credit.

Tax basis calculation

Real estate income - costs - expenses - incremental increase in value.

Incremental increase in value limit = current market value at time of previous property transfer.

Cost and Expense rules

The incremental value allowed to be deducted is limited to the amount accruing from the last property transaction, rather than the total change in value since the construction of the property was completed.

When applying for deductions, if documents showing costs are not provided, approved documents can be used to verify cost. The current value of any appraisal or publicly available land prices can be used after adjusting for changes in the consumer price index.

For individuals, expenses are limited to 3% of the total value of the transaction, and should not exceed NTD300,000. For profit-seeking enterprises expenses are limited to 3% of costs, and should not exceed NTD300,000.

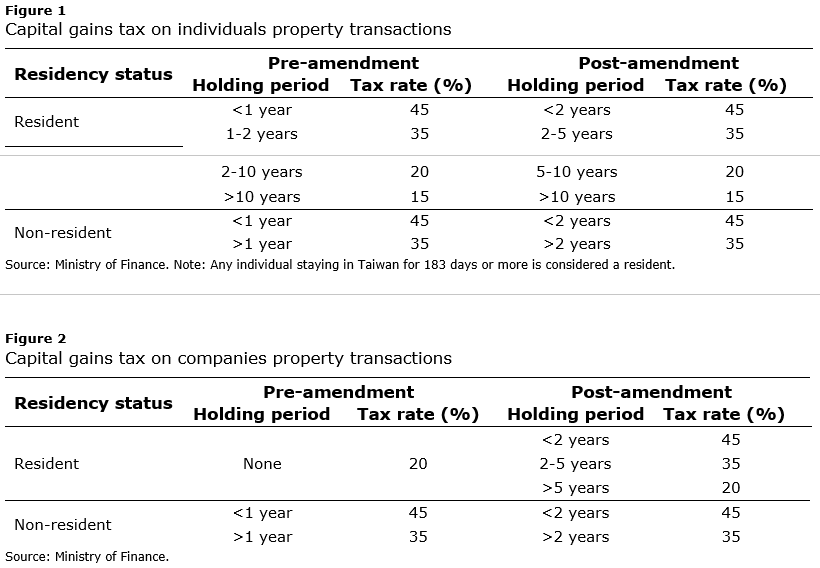

Higher rates

Individuals and companies must now pay rates based on longer holding periods, as in the charts below:

Unchanged rates

For the following five scenarios, the rate of capital gains tax is the same, and unless specified, applies to transactions involving individuals and profit-seeking enterprises.

Capital gains at 20%:

1. Forced transactions for reasons such as involuntary unemployment or enforcement of contract terms.

2. Transactions where the property sold is built on land owned by an individual or enterprise.

3. Transactions involving the renewal or reconstruction of a derelict or dangerous property.

4. The first transfer after an enterprise completes construction.

Capital gains at 10%:

5. Home owners who have lived in their own home for six years or more can deduct NTD4mn from the value of the transaction, with the remainder taxed at 10%.

Please add five types of transaction which maintains the same tax rates as before the amendment.

Expanded scope

The scope of the capital gains tax is broader, and now includes pre-sold property transactions, either with or without land. Relevant costs of acquisition can be deducted when calculating the capital gains tax amount. Prior to the amendments, these transactions were not taxed. In addition, the holding period for profit-seeking enterprises is calculated based on the legal person, with tax on properties being calculated separately.

Indirect property transfer

The amendments also require capital gains tax to be paid on share transactions where over 50% of the value of shares transacted are derived from Taiwanese properties, regardless of whether the shares are of a foreign company or a Taiwanese company. This excludes share sales of listed securities.

The bigger picture - Conclusion

These changes are part of a broader shift to target property tax evasion, and cool down a red hot property market. Other measures include an inspection targeting individuals with 10 or more properties and ongoing work with local authorities to raise the tax basis for non-owner occupied properties.

The overall trend is for continued tax reform and sustained oversight of tax avoidance. As such individuals with multiple properties or real estate companies are likely to be on the receiving end of further scrutiny. To avoid fines ranging from NTD30,000-50m, property owners must prepare the correct documents and be aware of the latest changes to the law.